Editor's Note

Mid-November 2025

Global mining has entered a decisive phase, marked by record-scale fiscal stimulus, direct state intervention, and the acceleration of “resource security” as a policy doctrine. Canada’s C$6.4 billion mining budget and sovereign fund are a pivotal competitive signal—shifting global investor expectations and placing renewed emphasis on tax incentives for critical minerals, project readiness, and allied supply chain resilience (Hidayat, 2025; Tomesco & McClelland, 2025). These fiscal measures have triggered a wave of corporate realignments and M&A, exemplified by Anglo American’s strategic tie-up with Teck and the rapid reallocation toward battery storage supply networks (McGee & Willis, 2025; Friedman, 2025).

Policy volatility and country-level mandates—from Canada’s emissions price overhaul to Africa’s assertive resource sovereignty and China’s shifting export controls—define the new anatomy of sectoral risk. Strategic capital now flows where regulatory frameworks align with competitive certainty and geopolitical leverage: the repositioning of battery and metals strategies, the redrawing of mineral exploration incentives, and the creation of partnership corridors between the North and the Global South (Rankin, 2025; Iragi, 2025). Investors and operators are compelled to treat bilateral agreements and regulatory pivots not as peripheral risks but as core drivers of portfolio value and deal velocity.

The events spotlighted in this mid-November report are more than market blips; they represent structural inflections reshaping equity valuations, deal activity, and supply chain architectures. Institutional investors, corporate strategists, and capital markets professionals must translate this turbulence into actionable foresight—cognizant that every policy turn, capital flow, and project milestone carries outsized implications for future value creation in mining and critical minerals (Smith, 2025; CBC News, 2025; Reuters, 2025).

Market Pulse

Macro sentiment: Budget windfall positions Canada as a global mining leader.

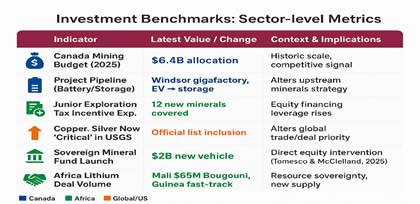

Canada announces C$6.4B investment in mining through 2025 Budget, supporting critical minerals and infrastructure expansion—immediate effect for capital flows, exploration, and ESG mandates (Hidayat, 2025).

Canada’s commitment goes beyond simple capital infusions: The federal budget introduces a new C$2B sovereign fund for critical minerals, provides C$372M over four years for the First and Last Mile Fund to accelerate near-term projects, and commits C$443M toward processing technologies and allied investments—an unprecedented integration of industrial policy, project finance, and technology support (Tomesco & McClelland, 2025).

Triple Flag Precious Metals records Toronto’s largest mining IPO since 2012, raising over $250M—signals robust institutional appetite even amid flat price action (Reuters, 2021).

Ottawa expands tax credits to 12 critical minerals—unlocks broader junior exploration and boosts project pipeline for battery metals and strategic resources (Rankin, 2025).

Northland Power shares drop sharply after dividend cut—yield risk registers in renewables, prompting reallocation signals across infrastructure portfolios (Kiladze, 2025).

Windsor’s gigafactory pivots from EVs to energy storage as demand shifts—battery deployment re-prioritized, altering upstream metals purchasing (Friedman, 2025).

New deals with graphite miners highlight Canadian push to break China’s grip on supply chains—immediate market and regulatory relevance (Friedman, 2025).

International

International competition is intensifying: Significant funding to Brazilian rare earth projects backed by the U.S., new Saudi investments targeting Canadian mining, and evolving market fortunes for rare earth projects in Greenland—all reflect a realignment of capital around critical supply vulnerabilities and regulatory arbitrage (Financial Post, 2025; Mining.com, 2025; Globe & Mail, 2025).

Global Critical Minerals List Expansion: The U.S. Geological Survey and Department of the Interior released a revised 2025 list of 60 critical minerals, now including copper and silver, with policymakers warning that any supply shock to these minerals would impose significant costs on core sectors. This list underscores the importance of nations securing independent supply chains, as China temporarily suspended new export controls on rare earths following recent bilateral talks (SupplyChainDive.com, 2025; FederalRegister.gov, 2025).

African and Emerging Market Moves: Ongoing expansion and regulatory reform in Morocco and Senegal were highlighted at major regional mining summits, with Morocco ranked as Africa’s top destination for new mining investment and eighth globally in May 2025. African nations are accelerating resource sovereignty initiatives—especially in lithium, gold, and alumina—altering raw material flows and the calculus for multinationals and investors (Mining.com, 2025).

Copper Supply Constraints: The International Copper Study Group’s recent downgrade of global mine supply growth projections points to deepening supply-demand imbalances, compounding pressures on copper prices and development timelines for strategic assets (CruxInvestor.com, 2025).

Industry Conferences Driving Deals: Global flagship events such as 121 Mining Investment London (Nov 17–18), The Mining Show in Dubai (Nov 17–18), and SIM Senegal (Nov 4–6) are convening senior executives and investors to accelerate partnerships, asset sales, and innovation, further shaping global deal flow for late 2025 and into 2026 (NMG.com, 2025; CanadianMiningMagazine.com, 2025)

Critical Chains Visual Intelligence

Deal Flow

·Simandou Project Launch: The Simandou iron ore project in Guinea made a landmark advance in November 2025, with the latest tranche of financing secured by a China- and consortium-backed partnership (Rio Tinto, Chinese SOEs, Winning Consortium). This strategic project represents the largest greenfield iron ore development in Africa and is forecast to deliver over 120 million tonnes per annum at peak, with initial exports planned by 2026. The launch signals a significant shift in global iron supply chains and introduces new competition to Australia’s iron ore dominance. Simandou’s ramp-up is expected to drive infrastructure buildouts in West Africa, generate high-impact mineral revenues for the Guinean government, and reshape capital allocations for major steel and mining investors worldwide (Mining.com, 2025; Financial Times, 2025).

Teck–Anglo American Merger: Teck Resources and Anglo American agreed to a merger of equals to form Anglo Teck, a new global mining leader valued at around $70 billion, headquartered in Vancouver (Teck, 2025; CBC, 2025). The combined entity will provide over 70% copper exposure, control six world-class copper assets, and deliver US$800 million in annual pre-tax synergies, with an additional US$1.4 billion in potential EBITDA from operational integration. Teck shareholders will receive 1.3301 Anglo American shares for each Teck share and will own 37.6% of the merged company, with the deal expected to close within 12–18 months, pending regulatory and shareholder approvals. This creates one of the world’s top five copper producers, repositioning Vancouver as a critical mining and capital hub.

Nouveau Monde Graphite & Domestic Processing: The Canadian federal government struck multiple deals with Nouveau Monde Graphite and allied juniors as templates for scaling up domestic processing infrastructure and securing graphite supply away from Chinese control (Friedman, 2025). These partnerships are central to Canada’s critical minerals industrial strategy, supporting new battery and EV supply chains, and providing capital to allow near-term project construction and offtake security for North American OEMs and allied partners.

Serra Verde & U.S.-backed Brazilian Rare Earths: Serra Verde secured $465 million in U.S. government and private funding to accelerate Brazil’s largest, rare earth deposit into production (Financial Post, 2025). The move marks intensified U.S. efforts to diversify high-value magnet material supply chains and reduce risk from China-driven volatility, directly boosting Western-aligned rare earths processing and export capacity.

Saudi–Canadian Investment Expansion: Saudi Arabia’s investment minister announced direct interest in new Canadian mining ventures, particularly in critical and strategic minerals (Globe & Mail, 2025). This rapidly expands the Gulf–Canada corridor as Riyadh diversifies away from hydrocarbons, providing Canadian juniors and infrastructure projects with deeper pools of partner capital and raising project selection competition for global investors.

Greenland Rare Earths Approvals: Greenland’s flagship rare earths project received key environmental approvals, opening the way for European and North American downstream users to tap new, non-Chinese sources of strategic materials (Mining.com, 2025). The move is critical as the EU and U.S. chase supply independence and motivates parallel investments in Arctic logistics and regional offtake agreements.

Canada Major Projects Office Fast-Tracks Key Approvals: The Major Projects Office announced approvals for a second tranche of strategic assets: Northcliff Resources’ tungsten project (New Brunswick), Nouveau Monde Graphite’s Quebec plant, and Canada Nickel’s Crawford Project (Ontario) (Mining.com, 2025; PM.gc.ca, 2025). Crawford features ultra-low-carbon nickel output, supporting Canada’s ESG credentials and competitive position in battery metals and low-footprint steel.

Table: Deal Flow Importance

Critical Chains Visual Intelligence

Geopolitical Watch

Regulatory risk: Policy shifts drive competitive alignment in mining corridors.

Canada’s budget launches sovereign fund for critical minerals, designed to secure supply chains and strategic equity positions—signals direct state market intervention (Tomesco & McClelland, 2025).

Federal government and partners launch First and Last Mile Fund—focus on near-term production acceleration, $372M allocated for strategic assets (Tomesco & McClelland, 2025).

Critical Mineral Exploration Tax Credit extended—defense and tech minerals now covered, influencing cross-sector capital deployment (Rankin, 2025).

Canada’s emissions regime revised; industrial tax rates nearly eliminated for processors, aiming net-zero by 2050—risk model recalibration required for all capex projections (CBC News, 2025).

African governments (Mali, Guinea, DRC) ramp resource sovereignty; lithium and alumina processing fast-tracked with UK/China capital—raises stakes for global operators and deal teams (Reuters, 2025).

China lifts restrictions for auto chip exports, while cobalt and lithium supply chains face new ecological compliance pressure in DRC—market risk acute for battery metals (Iragi, 2025)

Data Spotlight

Mid-November 2025 global mining sector market trends—each point represents a direct capital signal or a change in sector risk, informing strategy for institutional investors and corporate decision-makers.

Critical Chains Visual Intelligence

Looking Ahead

Get the complete monthly Critical Chains edition for deeper analysis, exclusive forecasts, and strategic briefings—subscribe or contact NM Advisory at info@novaminespr.com.

Powered by

Strategic communications, ESG advisory, and sector-specific political intelligence for mining, renewable energy, and Canadian capital markets—bridging Canada and Africa.

novaminespr.com

Sources

Financial Post. (2025, November). Various reports on global mining sector deal flow, rare earths, and Canadian policy developments.

Friedman, G. (2025, November). Reports on Windsor gigafactory pivot and graphite deals.

Hidayat, M. (2025, November). Analysis of Canada’s 2025 mining budget allocation and sector leadership.

Kiladze, T. (2025, November). Market analysis of Northland Power and Canadian yield dynamics.

Mining.com. (2025, November). Coverage of critical minerals list changes, Greenland project, and global supply trends.

Rankin, A. (2025, November). Coverage on junior exploration incentives and tax credit expansion.

Reuters. (2025, November). Analysis of Africa lithium deal volume and resource sovereignty trends.

Tomesco, F., & McClelland, C. (2025, November). Reports on Canada’s sovereign mineral fund launch and direct equity intervention.